CIO Views: Fixed income performance driven by lower rate expectations

- 03 Ottobre 2024 (3 min di lettura)

KEY POINTS

Chris Iggo, CIO AXA IM Core

Fixed income benefiting from lower rate expectations

Lower interest rate expectations – further confirmed by the Federal Reserve’s September cut - have helped drive recent strong fixed income performance. Returns for global government and corporate bonds over the third quarter have been among the strongest of the last 10 years. Going forward, bond yields may not be able to fall much further given what is already priced in. For rate expectations to decline further, the narrative would have to be that recessions risks are increasing or that a ‘neutral’ level for rates is even lower than previously thought. However, this is a low conviction view, given that recession signs are minimal so far. Forecasts of rates below 3% in the US and below 2% in Europe by the end of 2025 look to reflect the most likely macroeconomic outcomes.

As such, we believe the best way to access fixed income remains through yield curve steepening strategies, i.e. focusing on bonds towards the shorter end of the maturity spectrum. These should benefit from lower central bank interest rates. Additionally, corporate bonds remain attractive at current yields. Cash interest rates are set to fall below average yields on high grade corporate bonds, while high yield bonds provide a significant yield premium. Fundamentals in the corporate sector are solid and demand for higher yielding, income-generating assets remains strong. A consolidation of yields is not a negative sign for fixed income returns.

Alessandro Tentori, CIO Europe

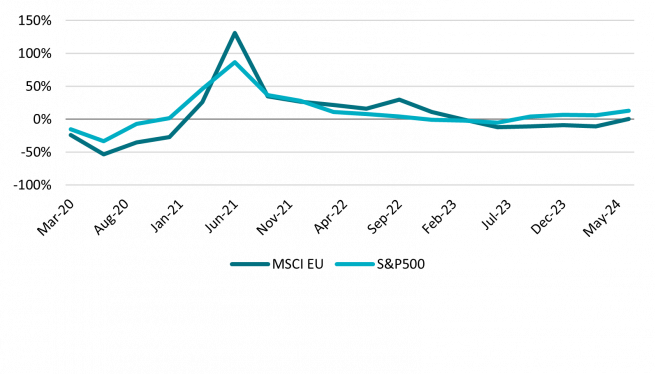

European equities: Improved earnings but still lagging the US

Following five quarters of negative earnings growth, European equities have crawled back into positive territory. And data measures suggest markets are bullish on European equities. However, absolute earnings growth still lags Wall Street by a considerable margin. Two factors could explain the 10 times price-to-earnings valuation gap between the MSCI US and MSCI EU indices.

Firstly, structural factors - relatively low productivity, regional fragmentation and implementation issues on European Union (EU) projects – such as the Banking Union - continue to depress Europe’s potential growth rate. The International Monetary Fund expects the US to grow almost twice as fast as Europe in the long run.

Secondly there’s sectoral differences. Looking at the historical composition of major indices, Europe seems to lag in industries like information technology. Some 20 years ago, the sector represented 16% of the S&P 500’s and 4% of the Stoxx 600’s market capitalisation. By the end of 2023, the share had increased to 29% in the US, but only to 7% in Europe. However, industrials and healthcare have gained in importance in the bloc since 2004.

Assuming artificial intelligence-based technology will dominate in the years to come, Europe’s specific industrial make-up might be a key factor both in terms of long-term macroeconomics and expected performance - a crucial issue highlighted by former European Central Bank President Mario Draghi’s recent report on EU competitiveness.

Ecaterina Bigos, CIO Asia ex-Japan

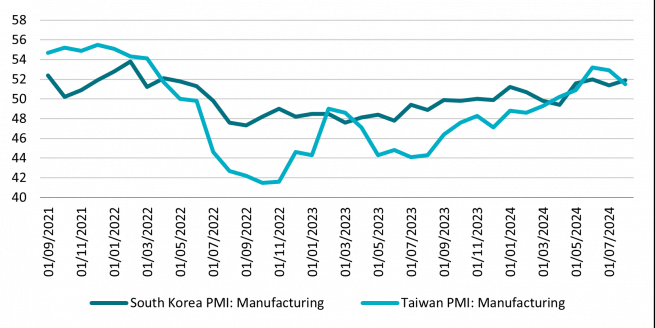

Asia-Pacific manufacturing holding up, powered by AI

Despite worries about artificial intelligence (AI) overhype, US capital goods imports remained robust over the past year, driven by industrial machines, computers, computer accessories and semiconductors - likely due to AI-related investment and spurred on by the 2022 CHIPS act. In contrast, consumer goods imports have largely returned to pre-pandemic levels.

This resilient investment in technology is supporting Asia’s tech trade. The initial winners of the investment cycle have been the enablers – infrastructure firms, storage providers and chipmakers. Asia ex-Japan has the highest share among the major regions of enabler companies, primarily in the semiconductor and hardware supply chain. Taiwan, followed by South Korea, are the market leaders and industry bellwethers.

Taiwan recorded sharp growth in chip exports of 89.8% year on year to September 2024, while South Korea’s rose by 44% over the same period. This has contributed to both countries’ manufacturing Purchasing Managers’ Indices staying resilient despite the global growth slowdown. The drivers are undoubtedly narrow and could be derailed if demand falters, but for now, with under-investing in AI perceived by many

corporates as a bigger risk than over-investing, the cycle likely has further to run.

Asset Class Summary Views

Views expressed reflect CIO team expectations on asset class returns and risks. Traffic lights indicate expected return over a three-to-six-month period relative to long-term observed trends.

| Positive | Neutral | Negative |

|---|

CIO team opinions draw on AXA IM Macro Research and AXA IM investment team views and are not intended as asset allocation advice.

Rates | Easing cycle in full swing but much is already priced in | |

|---|---|---|

US Treasuries | Market already priced for significant rate cuts in 2025 | |

Euro – Core Govt. | Little value right now with ECB rate cuts priced in | |

Euro – Peripherals | Presents opportunities and higher real yields than Bunds | |

UK Gilts | Interest rate cuts fully discounted; markets await fiscal plans | |

JGBs | Uncertainty over Bank of Japan policy normalisation path. Yen remains volatile | |

Inflation | Market pricing not discounting any post-election inflation shock |

Credit | Favourable pricing is increasing the asset class’s contribution to excess returns | |

|---|---|---|

USD Investment Grade | Without significant growth deterioration, credit to remain resilient | |

Euro Investment Grade | Resilient growth and lower interest rates support credit’s income appeal | |

GBP Investment Grade | Returns supported by better growth and expectations of rate cuts | |

USD High Yield | Narrative of growth without inflation is supportive. Fundamentals and funding remain strong | |

Euro High Yield | Strong fundamentals, technical factors and ECB cuts support total returns | |

EM Hard Currency | Higher quality universe, well-placed with US interest rate cuts commencing |

Equities | Soft landing to support stocks into year-end | |

|---|---|---|

US | Lower rates should sustain confidence in earnings | |

Europe | Attractive valuations, along with positive economic and earnings surprises | |

UK | Relatively more attractive valuations and positive economic momentum | |

Japan | Benefitting from semiconductor growth. Reforms and monetary policy in focus for broader performance | |

China | Policy announcements may lead to improved growth and market performance | |

Investment Themes* | Secular spending on technology and automation to support relative outperformance |

*AXA Investment Managers has identified six themes, supported by megatrends, that companies are tapping into which we believe are best placed to navigate the evolving global economy: Technology & Automation, Connected Consumer, Ageing & Lifestyle, Social Prosperity, Energy Transition, Biodiversity.

Disclaimer

Comunicazione di marketing: Prima dell’investimento in qualsiasi fondo gestito o promosso da AXA Investment Managers o dalle società ad essa affiliate, si prega di consultare il Prospetto e il Documento contenente le informazioni chiave per gli investitori (KID). Tali documenti, che descrivono anche i diritti degli investitori, possono essere consultati - per i fondi commercializzati in Italia - in qualsiasi momento, gratuitamente, sul sito internet www.axa-im.it e possono essere ottenuti gratuitamente, su richiesta, presso la sede di AXA Investment Managers. Il Prospetto è disponibile in lingua italiana e in lingua inglese. Il KID è disponibile nella lingua ufficiale locale del paese di distribuzione. Maggiori informazioni sulla politica dei reclami di AXA IM sono al seguente link: https://www.axa-im.it/avvertenze-legali/gestione-reclami. La sintesi dei diritti dell'investitore in inglese è disponibile sul sito web di AXA IM https://www.axa-im.com/important-information/summary-investor-rights.

I contenuti pubblicati nel presente sito internet hanno finalità informativa e non vanno intesi come ricerca in materia di investimenti o analisi su strumenti finanziari ai sensi della Direttiva MiFID II (2014/65/UE), raccomandazione, offerta o sollecitazione all’acquisto, alla sottoscrizione o alla vendita di strumenti finanziari o alla partecipazione a strategie commerciali da parte di AXA Investment Managers o di società ad essa affiliate, né la raccomandazione di una specifica strategia d'investimento o una raccomandazione personalizzata all'acquisto o alla vendita di titoli. L’investimento in qualsiasi fondo gestito o promosso da AXA Investment Managers o dalle società ad essa affiliate è accettato soltanto se proveniente da investitori che siano in possesso dei requisiti richiesti ai sensi del prospetto informativo in vigore e della relativa documentazione di offerta.

Il presente sito contiene informazioni parziali e le stime, le previsioni e i pareri qui espressi possono essere interpretati soggettivamente. Le informazioni fornite all’interno del presente sito non tengono conto degli obiettivi d’investimento individuali, della situazione finanziaria o di particolari bisogni del singolo utente. Qualsiasi opinione espressa nel presente sito internet non è una dichiarazione di fatto e non costituisce una consulenza di investimento. Le previsioni, le proiezioni o gli obiettivi sono solo indicativi e non sono garantiti in alcun modo. I rendimenti passati non sono indicativi di quelli futuri. Il valore degli investimenti e il reddito da essi derivante possono variare, sia in aumento che in diminuzione, e gli investitori potrebbero non recuperare l’importo originariamente investito.

Ancorché AXA Investment Managers impieghi ogni ragionevole sforzo per far sì che le informazioni contenute nel presente sito internet siano aggiornate ed accurate alla data di pubblicazione, non viene rilasciata alcuna garanzia in ordine all’accuratezza, affidabilità o completezza delle informazioni ivi fornite. AXA Investment Managers declina espressamente ogni responsabilità in ordine ad eventuali perdite derivanti, direttamente od indirettamente, dall’utilizzo, in qualsiasi forma e per qualsiasi finalità, delle informazioni e dei dati presenti sul sito.

AXA Investment Managers non è responsabile dell’accuratezza dei contenuti di altri siti internet eventualmente collegati a questo sito. L’esistenza di un collegamento ad un altro sito non implica approvazione da parte di AXA Investment Managers delle informazioni ivi fornite. Il contenuto del presente sito, ivi inclusi i dati, le informazioni, i grafici, i documenti, le immagini, i loghi e il nome del dominio, è di proprietà esclusiva di AXA Investment Managers e, salvo diversa specificazione, è coperto da copyright e protetto da ogni altra regolamentazione inerente alla proprietà intellettuale. In nessun caso è consentita la copia, riproduzione o diffusione delle informazioni contenute nel presente sito.

AXA Investment Managers può decidere di porre fine alle disposizioni adottate per la commercializzazione dei suoi organismi di investimento collettivo in conformità a quanto previsto dall'articolo 93 bis della direttiva 2009/65/CE.

AXA Investment Managers si riserva il diritto di aggiornare o rivedere il contenuto del presente sito internet senza preavviso.

A cura di AXA IM Paris – Sede Secondaria Italiana, Corso di Porta Romana, 68 - 20122 - Milano, sito internet www.axa-im.it.

© 2025 AXA Investment Managers. Tutti i diritti riservati.