China Outlook – Consumers key to breaking the deadlock

- 04 Dicembre 2024 (5 min di lettura)

Another bumpy journey to target

For China, achieving its annual economic growth target remains the central performance measure for officials at all levels. The economy was well on track to meet 2024’s goal of “around 5%” by the end of the first half of 2024, largely due to robust momentum from state-led investment. However, this positive trajectory was disrupted as local governments, perhaps overconfident from initial progress, or constrained by mounting debt pressures, slowed investment at the start of the third quarter. This decision triggered a broad-based economic slowdown. In response, Beijing reiterated its commitment to the growth target, and the central bank implemented stronger-than-expected monetary easing measures in late September. As a result, the economy now seems poised to meet this year’s growth objective.

Looking back, 2024’s bumpy path evokes a sense of déjà vu. The post-pandemic reopening boost provided a strong start to growth in the first half of 2023. Yet, policy support fell short of sustaining that momentum as the reopening effect waned. To stabilise growth, Beijing was compelled to unleash additional stimulus in October, including a rare mid-year budget adjustment that benefitted infrastructure investment. Ultimately, the economy managed to achieve its target, expanding by 5.2%.

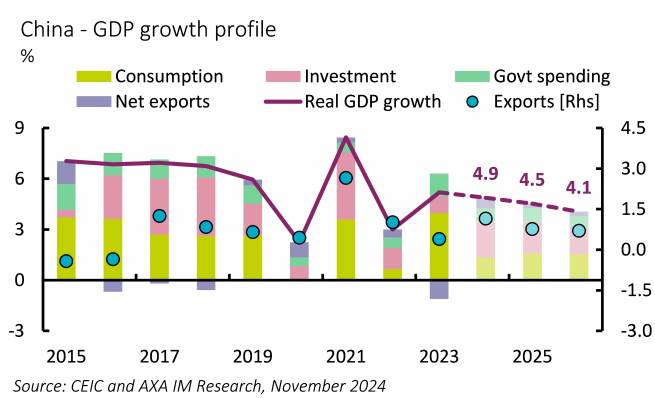

Many of the economic obstacles faced in 2024 carried over from 2023 and have since deepened further. To avoid a more material slowdown as domestic obstacles and external pressures look set to mount, China will remain heavily reliant on policy support. We foresee an ongoing need for additional fiscal stimulus and a shift in focus for its delivery – from production to consumer demand-centric. Assuming this, we predict a managed economic slowdown is ahead for China’s economy, forecasting growth of 4.5% in 2025 and 4.1% in 2026 (Exhibit 12). However, with Donald Trump’s return to the White House amplifying external risks and an already fragile domestic economy, a debt-deflation trap leading to a generational downturn could be perilously close if upcoming stimulus measures are delayed or misdirected.

Troubled consumers drag on the economy

Chinese consumers continued to struggle in 2024, as the triple impact of declining wealth, stagnating incomes and limited policy support underpinned entrenched pessimism.

Property prices continued their unprecedented adjustment, with average home values falling by 15% from their peak in the summer of 2021 – five percentage points (ppt) in 2024 – approximately a third of the total correction we estimated3 . The shrinking value of property assets – where Chinese households have historically concentrated most of their wealth – has placed significant strains on domestic consumers. This compounded the fading post-pandemic reopening momentum in the labour market, further dampening consumer spending. Although headline unemployment figures indicated a mild improvement from 2023 levels, they provide limited insights into broader labour market dynamics. Wage growth throughout 2024 was particularly lacklustre. Following divergent trends in 2023, 2024 saw even lower-income earners face stalling wages. The pervasive slowdown in wage growth, combined with a pessimistic income outlook has led consumers to become increasingly cautious in their spending habits.

Moreover, Beijing’s policy focuses on largely overlooked household demand for much of the year. It was not until Q3 2024 that the government began to acknowledge subdued household spending and rising deflationary risks, though substantial quantitative measures were still lacking. As a result, a robust recovery in domestic demand is yet to emerge, as reflected in persistently low consumer confidence levels.

Stronger headwinds from abroad

By contrast, Chinese exports have maintained a good momentum, particularly since the second quarter of this year. This in part stemmed from front-loading demand, as foreign importers sought to avoid potential higher tariffs on Chinese goods as the US, the European Union, Canada and Indonesia all raised tariffs on Chinese goods in 2024. However, Trump’s return to the White House once again threatens a more hostile external environment for China.

We do not anticipate Trump’s proposed 60% blanket tariff on Chinese imports being fully implemented. During his 2016 campaign, despite his calls for a 45% tariff on Chinese goods, only 37% of the claim was ultimately enacted. The resulting decline in China’s exports to the US cut China's GDP growth by 0.6ppt, including the partial offset from currency devaluation – the Chinese yuan depreciated 5.2% against the US dollar. In Trump’s second term, we foresee a similar materialisation rate for the tariff policy relative to his campaign rhetoric. This would suggest a comparable tariff rise to that seen in the 2018-2020 period, with a similar impact on China's GDP, assuming similar currency adjustment behaviours.

- e2h0dHBzOi8vd3d3LmF4YS1pbS5jb20vaW52ZXN0bWVudC1pbnN0aXR1dGUvbWFjcm9lY29ub21pY3MvbWFjcm9lY29ub21pYy1yZXNlYXJjaC9icmljay1icmljay11bnJhdmVsbGluZy1jaGluYXMtcHJvcGVydHktcHV6emxlO1dhbmcsIFkuLCZuYnNwO+KAnEJyaWNrIGJ5IEJyaWNrOiBVbnJhdmVsbGluZyBDaGluYQ==

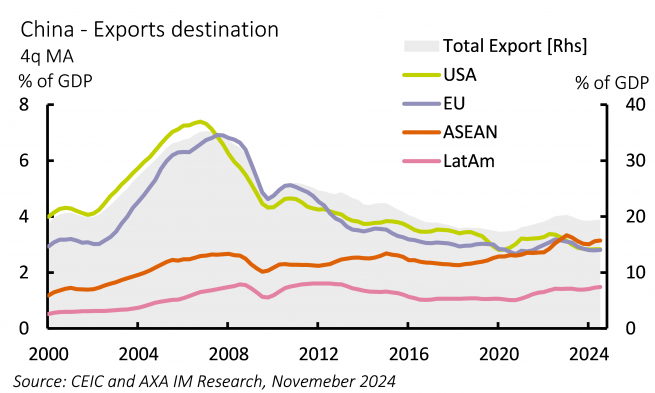

China has diverted its exports to other markets outside the US (Exhibit 13), and its integration into key global supply chains has deepened compared to 2018. These factors should offer some buffer against future potential US-China trade disruptions. It is worth noting the US’s broader trade policies with other countries could also have implications for China’s exports—harsher US trade stances globally may somewhat mitigate Chinese goods’ loss of competitiveness. Overall, we estimate that Trump’s anticipated trade policies will shave 0.3-0.5ppt off China’s GDP, although a large degree of uncertainty surrounds these projections.

Domestic spending may be the last resort

China’s investment-driven and export-supported growth model, which was instrumental in the nation’s remarkable growth over the past three decades, has long been a cornerstone of its economic policy. However, the conditions that once underpinned this success have shifted significantly. Although the recently announced RMB 10trn multi-year debt swap programme aims to alleviate mounting local government debt pressures4 , returns on investment have diminished, constraining their ability to sustain expansion. Moreover, the golden era of infrastructure growth has slowed, reflecting the plateauing of urbanisation and a cooling housing market. While exports have transitioned to higher-value, technologically advanced goods, escalating trade tensions and shifting geopolitical dynamics present growing obstacles.

This places greater emphasis on China’s households, which hold substantial growth potential due to one of the world’s highest saving rates. With the right policies to revive the labour market and stabilise the property sector, a portion of these savings could be unlocked, albeit rebalancing the economy to a consumption-driven growth will take time. Beyond recent challenges, the elevated savings rate stems from an incomplete and limited social safety net, underscoring the critical need for structural reforms. Implementing such reforms could take decades, and it remains uncertain whether the government is willing to undertake such a transformative agenda.

We consider a revival of domestic demand through household-focused stimulus as the most viable path to achieving a managed slowdown and avoiding a pernicious economic downturn. The National People’s Congress meeting in March next year looks the most likely juncture for additional stimulus. In the interim, authorities may also encourage state-owned enterprises to support employment and promote better wage growth. It would not only help facilitate a gradual slowdown in China’s economic growth over the coming years but could also underpin a modest rebound in consumer prices. Alongside the support from a weaker yuan, we forecast inflation to rise from near deflation this year to 1.0% in 2025 and 1.6% in 2026.

- PGEgaHJlZj0iaHR0cHM6Ly93d3cuYXhhLWltLmNvbS9pbnZlc3RtZW50LWluc3RpdHV0ZS9tYXJrZXQtdmlld3MvYm9uZHMtYnJpZGdlcy1hbmQtYnVyZGVucy1jaGluYXMtbG9jYWwtZ292ZXJubWVudC1kZWJ0LWZvY3VzIj5XYW5nLCBZLiwmbmJzcDvigJxCb25kcywgQnJpZGdlcywgYW5kIEJ1cmRlbnM6IENoaW5h4oCZcyBMb2NhbCBHb3Zlcm5tZW50IERlYnQgaW4gRm9jdXPigJ0sJm5ic3A7QVhBIElNIFJlc2VhcmNoLCBPY3RvYmVyIDIwMjQ8L2E+

Disclaimer

Prima dell’investimento in qualsiasi fondo gestito o promosso da AXA Investment Managers o dalle società ad essa affiliate, si prega di consultare il Prospetto e il Documento contenente le informazioni chiave per gli investitori (KID). Tali documenti, che descrivono anche i diritti degli investitori, possono essere consultati - per i fondi commercializzati in Italia - in qualsiasi momento, gratuitamente, sul sito internet www.axa-im.it e possono essere ottenuti gratuitamente, su richiesta, presso la sede di AXA Investment Managers. Il Prospetto è disponibile in lingua italiana e in lingua inglese. Il KID è disponibile nella lingua ufficiale locale del paese di distribuzione. Maggiori informazioni sulla politica dei reclami di AXA IM sono al seguente link: https://www.axa-im.it/avvertenze-legali/gestione-reclami. La sintesi dei diritti dell'investitore in inglese è disponibile sul sito web di AXA IM https://www.axa-im.com/important-information/summary-investor-rights.

I contenuti pubblicati nel presente sito internet hanno finalità informativa e non vanno intesi come ricerca in materia di investimenti o analisi su strumenti finanziari ai sensi della Direttiva MiFID II (2014/65/UE), raccomandazione, offerta o sollecitazione all’acquisto, alla sottoscrizione o alla vendita di strumenti finanziari o alla partecipazione a strategie commerciali da parte di AXA Investment Managers o di società ad essa affiliate, né la raccomandazione di una specifica strategia d'investimento o una raccomandazione personalizzata all'acquisto o alla vendita di titoli. L’investimento in qualsiasi fondo gestito o promosso da AXA Investment Managers o dalle società ad essa affiliate è accettato soltanto se proveniente da investitori che siano in possesso dei requisiti richiesti ai sensi del prospetto informativo in vigore e della relativa documentazione di offerta.

Il presente sito contiene informazioni parziali e le stime, le previsioni e i pareri qui espressi possono essere interpretati soggettivamente. Le informazioni fornite all’interno del presente sito non tengono conto degli obiettivi d’investimento individuali, della situazione finanziaria o di particolari bisogni del singolo utente. Qualsiasi opinione espressa nel presente sito internet non è una dichiarazione di fatto e non costituisce una consulenza di investimento. Le previsioni, le proiezioni o gli obiettivi sono solo indicativi e non sono garantiti in alcun modo. I rendimenti passati non sono indicativi di quelli futuri. Il valore degli investimenti e il reddito da essi derivante possono variare, sia in aumento che in diminuzione, e gli investitori potrebbero non recuperare l’importo originariamente investito.

Ancorché AXA Investment Managers impieghi ogni ragionevole sforzo per far sì che le informazioni contenute nel presente sito internet siano aggiornate ed accurate alla data di pubblicazione, non viene rilasciata alcuna garanzia in ordine all’accuratezza, affidabilità o completezza delle informazioni ivi fornite. AXA Investment Managers declina espressamente ogni responsabilità in ordine ad eventuali perdite derivanti, direttamente od indirettamente, dall’utilizzo, in qualsiasi forma e per qualsiasi finalità, delle informazioni e dei dati presenti sul sito.

AXA Investment Managers non è responsabile dell’accuratezza dei contenuti di altri siti internet eventualmente collegati a questo sito. L’esistenza di un collegamento ad un altro sito non implica approvazione da parte di AXA Investment Managers delle informazioni ivi fornite. Il contenuto del presente sito, ivi inclusi i dati, le informazioni, i grafici, i documenti, le immagini, i loghi e il nome del dominio, è di proprietà esclusiva di AXA Investment Managers e, salvo diversa specificazione, è coperto da copyright e protetto da ogni altra regolamentazione inerente alla proprietà intellettuale. In nessun caso è consentita la copia, riproduzione o diffusione delle informazioni contenute nel presente sito.

AXA Investment Managers può decidere di porre fine alle disposizioni adottate per la commercializzazione dei suoi organismi di investimento collettivo in conformità a quanto previsto dall'articolo 93 bis della direttiva 2009/65/CE.

AXA Investment Managers si riserva il diritto di aggiornare o rivedere il contenuto del presente sito internet senza preavviso.

A cura di AXA IM Paris – Sede Secondaria Italiana, Corso di Porta Romana, 68 - 20122 - Milano, sito internet www.axa-im.it.

© 2025 AXA Investment Managers. Tutti i diritti riservati.