Eurozone Outlook – Slowly taking off

- 04 Dicembre 2024 (5 min di lettura)

KEY POINTS

Modest growth acceleration with downside risks

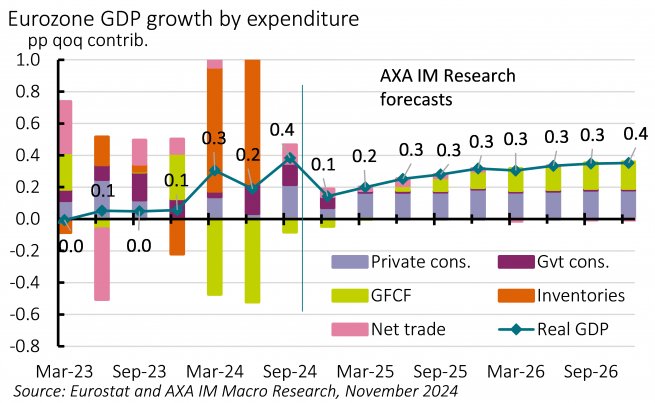

We expect the Eurozone’s protracted economic rebound to continue and given Q3’s stronger-than-expected performance we have revised our 2024 growth forecast up to 0.8% (up 0.1 percentage points). But beyond this, we maintain our below-consensus stance, projecting GDP growth at 1.0% in 2025 and 1.3% in 2026 (Bloomberg consensus: 1.2% and 1.4%). Our outlook is unchanged, anticipating expansion to recover slowly, led by private consumption in 2025, while investment should eventually make a firmer contribution in 2026.

Negotiated wage growth has exceeded inflation since Q3 2023, implying real purchasing power gains. However, the household saving rate has also been trending higher, culminating at 15.7% in Q2 2024, and acting as a brake to private consumption growth. Although we expect real wage growth to decelerate, we also anticipate some normalisation of the saving rate, implying a moderate but persistent pickup in consumer spending (Exhibit 7). However, the unprecedented recent savings behaviour makes it inherently difficult to forecast the timing and magnitude of such an acceleration.

We anticipate that investment will gently restart from the second half of 2025, following a year of progressive relaxation of monetary policy restrictiveness – and likely outright monetary easing to come – more than offsetting a reduced drag from profit margins.

Risks to our Eurozone growth forecasts are skewed to the downside. Trade policy and geopolitical uncertainty are running high after the US elections outcome. These come at a time when European political decisiveness is in question with several countries run by fragile coalitions. Notably, Germany is set to hold a general election on 23 February 2025, while snap elections in France and Spain cannot be ruled out. Increased political and economic uncertainty may imply that persistent manufacturing woes could spill over to services, leading to a quicker and more meaningful correction in the unemployment rate, projected to average 6.6% and 6.8% in 2025 and 2026 after 6.4% in 2024.

Inflation to stabilise below ECB’s target

Headline inflation markedly eased in 2024 and should average 2.3%, down from 5.5% in 2023. We see a continued shift from better supply conditions to weaker demand continuing to affect price dynamics. Due to this weak domestic demand outlook, we project inflation to stabilise at 1.9% in 2025 and 1.7% in 2026, below the European Central Bank’s (ECB) 2% target.

Eurozone core inflation should continue to edge down, to 2.1% in 2025 and 1.9% in 2026, from 2.8% this year. Though decelerating, we see services prices remaining the main inflation driver. By contrast, we foresee a pick-up of goods inflation pushing higher to 1.1% in 2025 and 1.3% in 2026 from 0.9% this year. We also expect food inflation to stabilise at its current level of around 3%, while the contribution from energy is expected to be slightly negative as market price futures continue to point to a weaker outlook. Such dynamics are likely to be only partially offset by the further expiry of energy crisis government support measures.

Towards an accommodative monetary policy stance

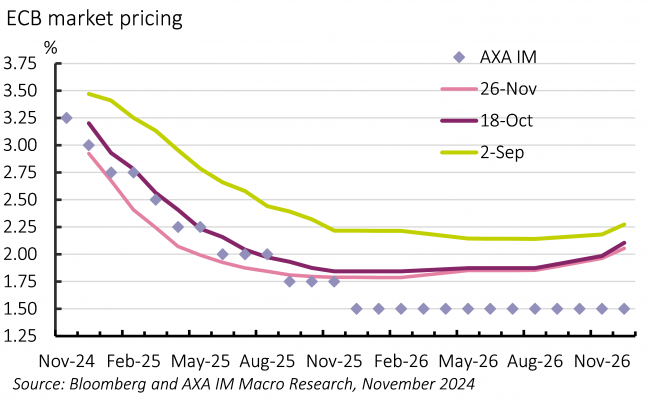

Our Eurozone sequential 2025 growth forecast (0.27% quarter-on-quarter on average) remains below estimates of potential growth (0.33%). Coupled with an undershoot of the ECB’s inflation target for most of 2025, there is an obvious case for a continued unwinding of the central bank’s restrictive stance. We continue to expect back-to-back 25-basis-point deposit rate cuts to reach 2.0% by next June, close to the vicinity of neutral rate territory.

Our projected path for 2026 sees a modest acceleration to potential growth, consistent with a continued undershooting of inflation (1.7%). This should push the ECB towards an accommodative policy stance. We expect it will cut twice in the second half of 2025, bringing the deposit rate to 1.5%, below current market pricing (Exhibit 8). Given the downside risks to growth, we think this could come sooner than end-2025, with the ECB forced into more accommodative territory.

There are two reasons that are likely to make the ECB more proactive in its policy response. First, compared with past years, weak Eurozone growth has rebalanced from supply to demand factors, on which the ECB can have more bearing via changes in its interest rate policy. Second, during the move towards a more accommodative stance, ECB risk management may encourage aggressive action to avoid being eventually pushed into extra-ordinary measures, including negative interest rates and/or quantitative easing.

Despite minor funding pressures arising, we do not think that the ECB is likely to alter the pace of balance sheet reduction, with excess liquidity projected to land at around €2.5tn by end-2026, still well above pre-pandemic levels. That said, we will watch for further details on the long-term aspects of the ECB’s operational review, including prospects for long-term liquidity injections and structural bond portfolios.

Fiscal policy: France to remain in the spotlight

The Eurozone’s stretched public finances will remain in focus across the bloc. However, for the first time in four years, countries have submitted budget plans following the application of (revised) EU rules after four years of suspension.

Nevertheless, we doubt the Eurozone’s fiscal stance will be as restrictive as suggested in these plans – Germany’s general election should offer an example of this. Moreover, several member states’ budgets have been built on optimistic growth assumptions, likely leading to slippage versus targets, notably France – the European Commission’s autumn forecasts concur. Finally, Italy and Spain are scheduled to receive increased amounts of Recovery and Resilience Facility funds next year.

Furthermore, France and Italy’s public debt-to-GDP ratios are rising due to delayed deficit reduction, reflecting a challenging planned adjustment for the former while still accounting for the ‘superbonus’ tax credit for the latter. This highlights the vulnerability of these two countries – and the Eurozone as a whole – in case these downside risks to growth materialise.

Politics: No momentum to address key issues

German Chancellor Olaf Scholz ended the country’s traffic-light coalition, calling for a snap election on 23 February 2025 – nine months ahead of schedule. Current polls show a likely CDU/CSU and SPD coalition return, although it is uncertain whether they will have enough votes to muster an outright majority in Parliament. It is not our base case scenario that Germany’s fiscal stance turns accommodative – a two-thirds Parliamentary majority required to overturn the debt brake rule looks prohibitive – rather, we envisage a slightly less restrictive stance. In sum, these elections are unlikely to prove a game changer for domestic, nor European, prospects.

Fragile government coalitions also exist in France and Spain; such that we cannot rule out snap elections in either over the next couple of years. These developments also emphasise the weakness to the new European Commission.

This puts Europe in a weak political and policy position when facing the renewed economic challenges, it’s likely to encounter from a new Donald Trump US presidency. Tariff hikes, domestic or global, could add to longstanding economic challenges including demographics, competitiveness and low productivity growth. Weak governments in key capitals could also increase the challenge of effective responses to arising geopolitical issues, of which Ukraine may be uppermost for Europe, but may also include the Middle East and climate change challenges.

Disclaimer

Comunicazione di marketing: Prima dell’investimento in qualsiasi fondo gestito o promosso da AXA Investment Managers o dalle società ad essa affiliate, si prega di consultare il Prospetto e il Documento contenente le informazioni chiave per gli investitori (KID). Tali documenti, che descrivono anche i diritti degli investitori, possono essere consultati - per i fondi commercializzati in Italia - in qualsiasi momento, gratuitamente, sul sito internet www.axa-im.it e possono essere ottenuti gratuitamente, su richiesta, presso la sede di AXA Investment Managers. Il Prospetto è disponibile in lingua italiana e in lingua inglese. Il KID è disponibile nella lingua ufficiale locale del paese di distribuzione. Maggiori informazioni sulla politica dei reclami di AXA IM sono al seguente link: https://www.axa-im.it/avvertenze-legali/gestione-reclami. La sintesi dei diritti dell'investitore in inglese è disponibile sul sito web di AXA IM https://www.axa-im.com/important-information/summary-investor-rights.

I contenuti pubblicati nel presente sito internet hanno finalità informativa e non vanno intesi come ricerca in materia di investimenti o analisi su strumenti finanziari ai sensi della Direttiva MiFID II (2014/65/UE), raccomandazione, offerta o sollecitazione all’acquisto, alla sottoscrizione o alla vendita di strumenti finanziari o alla partecipazione a strategie commerciali da parte di AXA Investment Managers o di società ad essa affiliate, né la raccomandazione di una specifica strategia d'investimento o una raccomandazione personalizzata all'acquisto o alla vendita di titoli. L’investimento in qualsiasi fondo gestito o promosso da AXA Investment Managers o dalle società ad essa affiliate è accettato soltanto se proveniente da investitori che siano in possesso dei requisiti richiesti ai sensi del prospetto informativo in vigore e della relativa documentazione di offerta.

Il presente sito contiene informazioni parziali e le stime, le previsioni e i pareri qui espressi possono essere interpretati soggettivamente. Le informazioni fornite all’interno del presente sito non tengono conto degli obiettivi d’investimento individuali, della situazione finanziaria o di particolari bisogni del singolo utente. Qualsiasi opinione espressa nel presente sito internet non è una dichiarazione di fatto e non costituisce una consulenza di investimento. Le previsioni, le proiezioni o gli obiettivi sono solo indicativi e non sono garantiti in alcun modo. I rendimenti passati non sono indicativi di quelli futuri. Il valore degli investimenti e il reddito da essi derivante possono variare, sia in aumento che in diminuzione, e gli investitori potrebbero non recuperare l’importo originariamente investito.

Ancorché AXA Investment Managers impieghi ogni ragionevole sforzo per far sì che le informazioni contenute nel presente sito internet siano aggiornate ed accurate alla data di pubblicazione, non viene rilasciata alcuna garanzia in ordine all’accuratezza, affidabilità o completezza delle informazioni ivi fornite. AXA Investment Managers declina espressamente ogni responsabilità in ordine ad eventuali perdite derivanti, direttamente od indirettamente, dall’utilizzo, in qualsiasi forma e per qualsiasi finalità, delle informazioni e dei dati presenti sul sito.

AXA Investment Managers non è responsabile dell’accuratezza dei contenuti di altri siti internet eventualmente collegati a questo sito. L’esistenza di un collegamento ad un altro sito non implica approvazione da parte di AXA Investment Managers delle informazioni ivi fornite. Il contenuto del presente sito, ivi inclusi i dati, le informazioni, i grafici, i documenti, le immagini, i loghi e il nome del dominio, è di proprietà esclusiva di AXA Investment Managers e, salvo diversa specificazione, è coperto da copyright e protetto da ogni altra regolamentazione inerente alla proprietà intellettuale. In nessun caso è consentita la copia, riproduzione o diffusione delle informazioni contenute nel presente sito.

AXA Investment Managers può decidere di porre fine alle disposizioni adottate per la commercializzazione dei suoi organismi di investimento collettivo in conformità a quanto previsto dall'articolo 93 bis della direttiva 2009/65/CE.

AXA Investment Managers si riserva il diritto di aggiornare o rivedere il contenuto del presente sito internet senza preavviso.

A cura di AXA IM Paris – Sede Secondaria Italiana, Corso di Porta Romana, 68 - 20122 - Milano, sito internet www.axa-im.it.

© 2025 AXA Investment Managers. Tutti i diritti riservati.